Energy Under Siege: Triple-Digit Oil and the Strategic Deadlock in the Strait of Hormuz

The Strait of Hormuz remains partially operational but heavily disrupted amid escalating maritime security incidents, placing approximately 20% of globally traded oil and liquefied natural gas flows under acute geopolitical risk and threatening procurement continuity across energy-intensive industries.

Brent crude benchmarks have been amplified toward triple-digit thresholds by converging supply-side constraints, redirected tanker traffic, and elevated war-risk insurance premiums compressing refining margins and fragmenting spot market reliability for downstream buyers.

Interdependencies between Hormuz passage volumes and Asian energy import dependencies have cascaded into power generation cost escalations and industrial input disruptions across South and East Asian manufacturing corridors, reshaping long-term supply chain exposure.

Supply Wisdom recommends real-time, continuous monitoring of maritime chokepoint disruptions, tanker routing anomalies, and energy price volatility events, as well as any other disruptions that could affect operations, given today's complex regulatory landscape. Read on for key insights into Hormuz-driven vulnerabilities reshaping global energy supply chains, procurement strategies, and industrial operations.

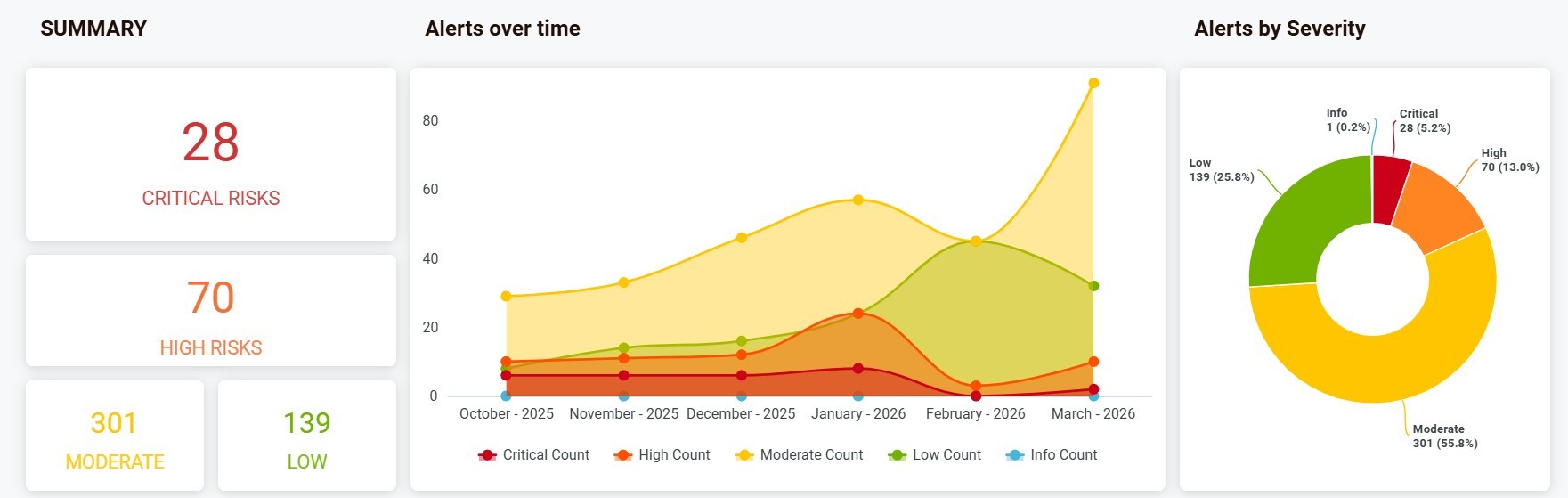

Key Findings

Tanker Routing and Freight Cost Disruption: Chokepoint dependency has fragmented global tanker routing reliability. Vessel operators reroute around the Cape of Good Hope, extending transit times by 10-20 days and driving VLCC (Very Large Crude Carriers) Middle East to China rates to ~US$420,000-424,000 per day, up from roughly ~US$120,000 per day prior to the escalation, materially elevating costs for Asian refiners and European energy importers.

War-Risk Insurance and Landed Cost Surge: War-Risk insurance premiums have subordinated shipping economics, with Lloyd's of London (Lloyd's) and affiliated markets pricing hull and cargo risk surcharges that are elevating landed energy cost structures for downstream industrial consumers. Lloyd's rates increased from ~0.25% before the 2026 Middle East escalation to up to ~1% of total hull value in early March 2026.

OPEC+ Spare Capacity and Price Floor Amplification: OPEC+ (Organization of the Petroleum Exporting Countries and allies) production discipline has amplified price floor mechanisms by curtailing spare capacity to ~5.6 million barrels per day (b/d) (down from pre-2023 peaks above 7 million b/d). This reduces spare capacity buffers, leaving ~20 million b/d of petroleum flows, about 20% of global liquids, vulnerable to potential disruption in the Strait of Hormuz. These factors sustain upward pressure on Brent and WTI (West Texas Intermediate) benchmarks toward triple-digit levels.

LNG Spot Liquidity and Delivery Fragmentation: Liquefied Natural Gas (LNG) spot market liquidity has been curtailed by diversion pressures, as Qatari and United Arab Emirates (UAE) export volumes faced scheduling uncertainty. This has fragmented contracted delivery windows for European and Asian utilities dependent on flexible spot procurement, particularly as Liquefied Natural Gas tanker rates surged over 40% to approximately US$62,000 per day and the Japan Korea Marker (JKM) benchmark doubled.

Downstream Petrochemical and Fertilizer Cost Cascade: Downstream petrochemical and fertilizer supply chains have cascaded into input cost inflation, as naphtha and gas feedstock disruptions propagated through polymer, plastics, and agricultural input sectors reliant on Gulf-origin hydrocarbon derivatives.

IEA (International Energy Agency) Reserve Drawdowns vs. Persistent Chokepoint Risk: IEA member states' Strategic Petroleum Reserve (SPR) drawdowns have provided partial price mitigation; yet structural chokepoint exposure remains unresolved. This subordinates medium-term energy security planning to geopolitical resolution timelines beyond commercial actors' control. For instance, coordinated SPR releases in early 2026 capped Brent price spikes temporarily. Still, with substantial Hormuz flows at risk, reserves deplete rapidly without alternative routes, forcing refiners to bid up spot cargoes amid VLCC constraints.

Source: Supply Wisdom Alerts covering Middle East’s Business Disruption/ Shutdown, Energy Crisis, Sabotage of Critical Infrastructure, Operational Costs, Pricing Surge, and Resource Shortage/Suspension of Services/Products from Octobe 01, 2025, to March 10, 2026

Value of Continuous Monitoring

Continuous, real-time monitoring of Hormuz transit data, tanker AIS (Automatic Identification System) positioning anomalies, and Gulf maritime incident reports lets procurement and supply chain teams spot supply cut signals days before oil price benchmarks fully show disruption severity. Multi-source intelligence covering geopolitical events, freight rates, insurance signals, and government energy policy updates, helps firms separate short-term swings from lasting chokepoint damage, adjusting hedges as needed.

Early signs of rerouting decisions by major tanker operators provide actionable lead time to activate alternative sourcing protocols and renegotiating delivery terms before spot market tightening constrains optionality. Ongoing tracking also reveals downstream effects, like falling refinery use in India, South Korea, and Japan that translate upstream Hormuz stress into downstream procurement exposure with greater precision than lagging price signals alone.

Cascading Risk Implications

The analysis moves beyond a single event assessment to illustrate how persistent structural factors converge to create acute single-point-of-failure conditions. These factors include chronic underinvestment in alternative transit infrastructure, a lack of unified maritime security in the Gulf, and reliance on a concentrated and aging global tanker fleet. The interaction of these vulnerabilities demonstrates how maritime security deterioration and geopolitical escalation can cascade across energy, logistics, and industrial domains, amplifying global supply chain risks and underscoring elevated operational fragility across energy-intensive sectors.

Monitoring indicators such as tanker rerouting patterns, war-risk insurance premiums, and OPEC+ spare capacity dynamics provides early signals of disruption escalation. Tracking these indicators enables procurement and risk teams to anticipate freight cost increases, tightening tanker availability, and heightened energy price volatility before these pressures fully materialize in spot markets. This forward-looking monitoring provides lead time to strengthen resilience protocols and diversify dependencies before acute disruption threatens strategic asset security and contractual commitments.

Supply Wisdom Alerts

Below are some of the alerts issued by Supply Wisdom that reflect real-time risk intelligence related to the ongoing conflict in the Middle East:

Critical Impact

March 2026:

Multiple Countries - Iran Declares Closure of Strait of Hormuz; Shipping Disruptions and Tankers Set Ablaze as Middle East Conflict Intensifies - Oil & Gas Prices Surge Globally

High Impact

March 2026:

Asia - Fuel Crisis Reported Amid Plunging Middle East Exports via the Strait of Hormuz - Multiple Governments Issues Energy-Saving Order, Educational Institutions Closed, and Price Cap on Petroleum Products Announced

Multiple Countries - Operational Disruptions Reported as Energy Companies Invoke Force Majeure and Suspend Shipments Amid Middle East War

Asia - Faces Fuel Oil Shortage as Middle East Exports Plunge Through Strait of Hormuz - Singapore Set for Further Oil Price Hikes, Raising Refueling Costs for Vessel Owners

Moderate Impact

March 2026:

Multiple Countries - Stock Markets Fall as Oil Price Surge Above US$100 Due to Middle East War - Japan’s Nikkei Down 6.2%, South Korea’s KOSPI 6.3%, Australia, New Zealand and Vietnam Indices over 3%

India - Operational Disruptions Reported Due to Commercial Liquefied Petroleum Gas Shortage Amid Middle East Tensions - Hotel and Restaurant Industry Faces Potential Shutdown

Multiple Countries - Saudi Aramco Issues Rare Crude Oil Tenders Amid Export Disruptions Linked to Iran Conflict

Pakistan - Energy Crisis Concerns Rise as Iran War Drives Fuel Price Surge and Cost Pressures

Pakistan - Government Raises Fuel Prices by ~20% Following Surge in Global Oil Costs Amid Middle East Conflict

Multiple Countries - Airfares Projected to Rise Due to Surge in Jet Fuel Prices Amid Middle East Conflict - Impact on Tourism, Travel, and Global Economic Activity Anticipated

GCC – Gulf Cooperation Council - Iran Launches Multiple Drone and Missile Attacks Across Region in Response to Continued Strikes by US and Israel - Several Oil Tankers Destroyed and Death Toll of 1,230 Reported

Bangladesh - Government Issues Cautionary Notes on Energy Usage Amid Middle East Conflict - Business Disruption Anticipated and Advises Citizens to Reduce Unnecessary Travel and Minimize Electricity Usages

Iran - Strait of Hormuz Remains Open; Iranian Navy Says Ships Managed Under International Protocols

Multiple Countries - Iran Closes Strait of Hormuz, Halting Global Oil Shipments Amid Tensions with US and Israel

February 2026:

Iran - Partial and Temporary Closure of ‘Strait of Hormuz’ over Security Precautions Amid Escalating Tensions with the US

Iran - Launches Military Drill in Strait of Hormuz Following US Aircraft Carrier Deployment Amid Escalating Tensions

Low Impact

March 2026:

Asia - Regional Currencies Weaken Against US Dollar Amid Middle East Tensions and Rising Oil Prices

Nigeria - Petrol Price Hikes over Global Oil Market Pressures and Middle East Conflicts

India - US Grants 30-Day Waiver Allowing Purchase of Russian Oil Amid Iran Conflict and Global Supply Concerns

China - Government Instructs Oil Refiners to Suspend Fuel Exports to Secure Domestic Supply Amid Middle East Conflict

India - Indian Rupee Declines to ₹92.15 Against US Dollar Amid Geopolitical Tensions and Surge in Oil Prices

A.P. Moller-Maersk - Suspends Vessel Transit Through Strait of Hormuz and Suez Canal Amid Escalating Regional Security Risks

Recap

Sustained maritime security pressures along the Strait of Hormuz have subordinated the reliability of approximately one-fifth of globally traded crude oil and LNG volumes, fragmenting procurement continuity for energy importers across Asia, Europe, and beyond. Tanker rerouting around the Cape of Good Hope has extended transit timelines and cascaded freight cost escalations into refiner margins and industrial input budgets. Simultaneously, OPEC+ production discipline has curtailed spare capacity buffers, amplifying oil price trajectories toward triple-digit thresholds and compressing the commercial flexibility available to downstream buyers navigating spot market tightening.

Asian energy import dependencies concentrated across South Korean, Japanese, Indian, and Chinese refining systems have been amplified by LNG spot market disruptions, propagating power generation cost pressures into manufacturing competitiveness. War-risk insurance surcharges have further fragmented tanker economics, elevating barriers for smaller operators and concentrating transit risk within a narrowing pool of capable fleet holders. Strategic petroleum reserve interventions coordinated through IEA member states have provided partial price dampening without resolving the structural chokepoint exposure that continues to subordinate medium-term energy security planning.

Organizations with energy-intensive supply chains or Gulf-region procurement dependencies must prioritize continuous monitoring of Hormuz transit conditions, tanker routing anomalies, and insurance market signals to maintain early-warning capability. Diversifying energy sourcing pathways, accelerating forward contract coverage, and stress-testing procurement models against prolonged rerouting scenarios remain critical actions to reduce fragility before acute disruption cascades into irreversible contractual and operational consequences.